MCA vide its notification dated 20th September, 2022, made amendments to the Companies (Corporate Social Responsibility Policy) Rules, 2016. These rules may be called as Companies (Corporate Social Responsibility Policy) Amendment, Rules, 2022. This Notification will come into force from the date of publication in Official Gazette.

| Sr. No. | Part/Chapter/Section /Sub-section(s) in the Companies Rules, 2014 Modifications | Part/Chapter/Section /Sub-section(s) in the Companies Rules, 2014 Modifications | Analysis |

| 1. | in rule 3, – in sub-rule (1), after the proviso, the following proviso shall be inserted | “Provided further that a company having any amount in its Unspent Corporate Social Responsibility Account as per sub-section (6) of section 135 shall constitute a CSR Committee and comply with the provisions contained in sub-sections (2) to (6) of the said section.”; | Every company including its holding or subsidiary, and a foreign company defined under clause (42) of section 2 of the Act having its branch office or project office in India, which fulfills the criteria specified in sub-section (I) of section 135 of the Act shall comply with the provisions of section 135 of the Act and these rules: Provided that net worth, turnover or net profit. of a foreign company of the Act shall be computed in accordance with balance sheet and Profit and loss account of such company prepared in accordance with the provisions of clause (a) of sub-section (1) of section 381 and section 198 of the Act. Provided further that a company having any amount in its Unspent Corporate Social Responsibility Account as per sub-section (6) of section 135 shall constitute a CSR Committee and comply with the provisions contained in sub-sections (2) to (6) of the said section. |

| sub-rule (2) shall be omitted. | |||

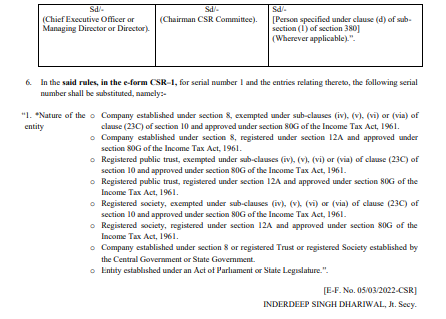

| 2. | in rule 4, for sub-rule (1), the following sub-rule shall be substituted | ‘(1) The Board shall ensure that the CSR activities are undertaken by the company itself or through, – (a) a company established under section 8 of the Act, or a registered public trust or a registered society, exempted under sub-clauses (iv), (v), (vi) or (via) of clause (23C) of section 10 or registered under section 12A and approved under 80 G of the Income Tax Act, 1961 (43 of 1961), established by the company, either singly or along with any other company; or (b) a company established under section 8 of the Act or a registered trust or a registered society, established by the Central Government or State Government; or (c) any entity established under an Act of Parliament or a State legislature; or (d) a company established under section 8 of the Act, or a registered public trust or a registered society, exempted under sub-clauses (iv), (v), (vi) or (via) of clause (23C) of section 10 or registered under section 12A and approved under 80 G of the Income Tax Act, 1961, and having an established track record of at least three years in undertaking similar activities. | A company established under section 8 of the Act, or a registered public trust or a registered society which has exemption under sub-clauses (iv), (v), (vi) or (via) of clause (23C) of section 10 along with approval under 80G shall be eligible to undertake CSR activities on behalf of other companies. Further, an explanation is added to clarify the meaning of the term “entity” under clause (c). |

| 3. | in rule 8, in sub-rule (3), in clause (c),- | (i) for the words “five percent”, the words “two per cent.” shall be substituted; (ii) for the words “whichever is less”, the words “whichever is higher” shall be substituted | A Company undertaking impact assessment may book the expenditure towards Corporate Social Responsibility for that financial year, which shall not exceed two percent of the total CSR expenditure for that financial year or fifty lakh rupees, whichever is higher. |

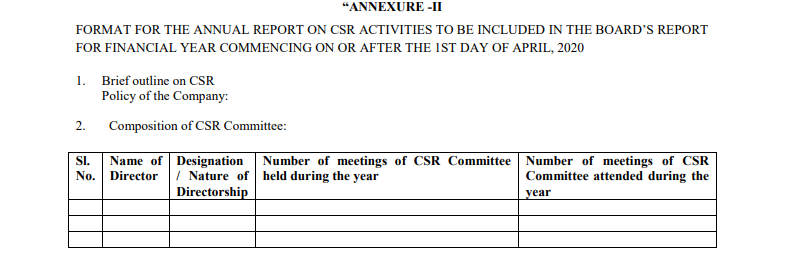

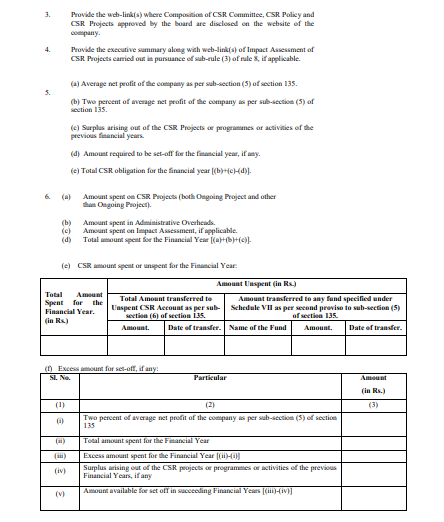

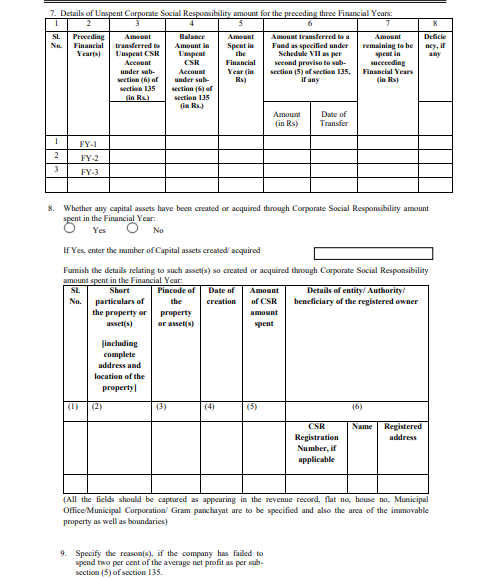

In the said rules, for Annexure-II, the following Annexure shall be substituted, namely:-

| Link to the Notification: |

| https://www.mca.gov.in/bin/dms/getdocument?mds=1Wt3uUYzV0rGCr2Vxa8ztQ%253D%253D&type=open |